TL;DR: Resolution No. 281 of 2025 reduced the mandatory e-invoicing registration threshold from EGP 500,000 to EGP 250,000 in annual revenue. Every business above this limit must register with the Egyptian Tax Authority (ETA) before March 31, 2026. Non-compliance triggers an immediate EGP 20,000 fine plus EGP 1,000 daily penalty, along with a new three-tier enforcement regime that can ultimately suspend your ability to issue valid invoices. This guide explains the difference between e-invoices and e-receipts, who must register, the complete technical integration path, and how to automate compliance end-to-end.

What Changed in Egypt’s ETA System in 2026?

The Egyptian Tax Authority (ETA) introduced three major regulatory shifts effective January 1, 2026 — the most significant updates since the e-invoicing mandate launched in 2020. If you operate a small or medium-sized business in Egypt, these changes directly affect your tax exposure.

1. Registration Threshold Dropped to EGP 250,000

Under Resolution No. 281 of 2025, the minimum annual revenue threshold for mandatory VAT and e-invoicing registration was cut in half — from EGP 500,000 down to EGP 250,000. This single change brings tens of thousands of small businesses, sole proprietorships, and freelance service providers into the mandate for the first time. If your 2025 revenue exceeded this figure, you have until March 31, 2026 to register.

2. Three-Tier Escalating Penalty Regime

Flat fines are gone. ETA now applies a graduated penalty system based on how many times you’ve submitted invoices late within a 12-month window. At the most severe level, the authority can suspend your ability to issue valid invoices altogether — effectively freezing all B2B transactions until you clear the backlog.

3. Mandatory QR Code on Printed E-Receipts

Starting 2026, every printed e-receipt must display a QR code that links back to the validated receipt record in the ETA portal. This allows consumers and tax inspectors to verify authenticity instantly via smartphone. In practice, it eliminates any possibility of issuing unauthorized receipts without immediate detection during routine audits.

4. Link to the Simplified Tax Regime

Law No. 6 of 2025 created a simplified tax regime for businesses earning under EGP 20 million annually. However, enrollment in both the e-invoice and e-receipt systems is a strict prerequisite for benefiting from this regime. Non-compliance automatically excludes your business from the simpler filing framework — forcing you back into full corporate reporting.

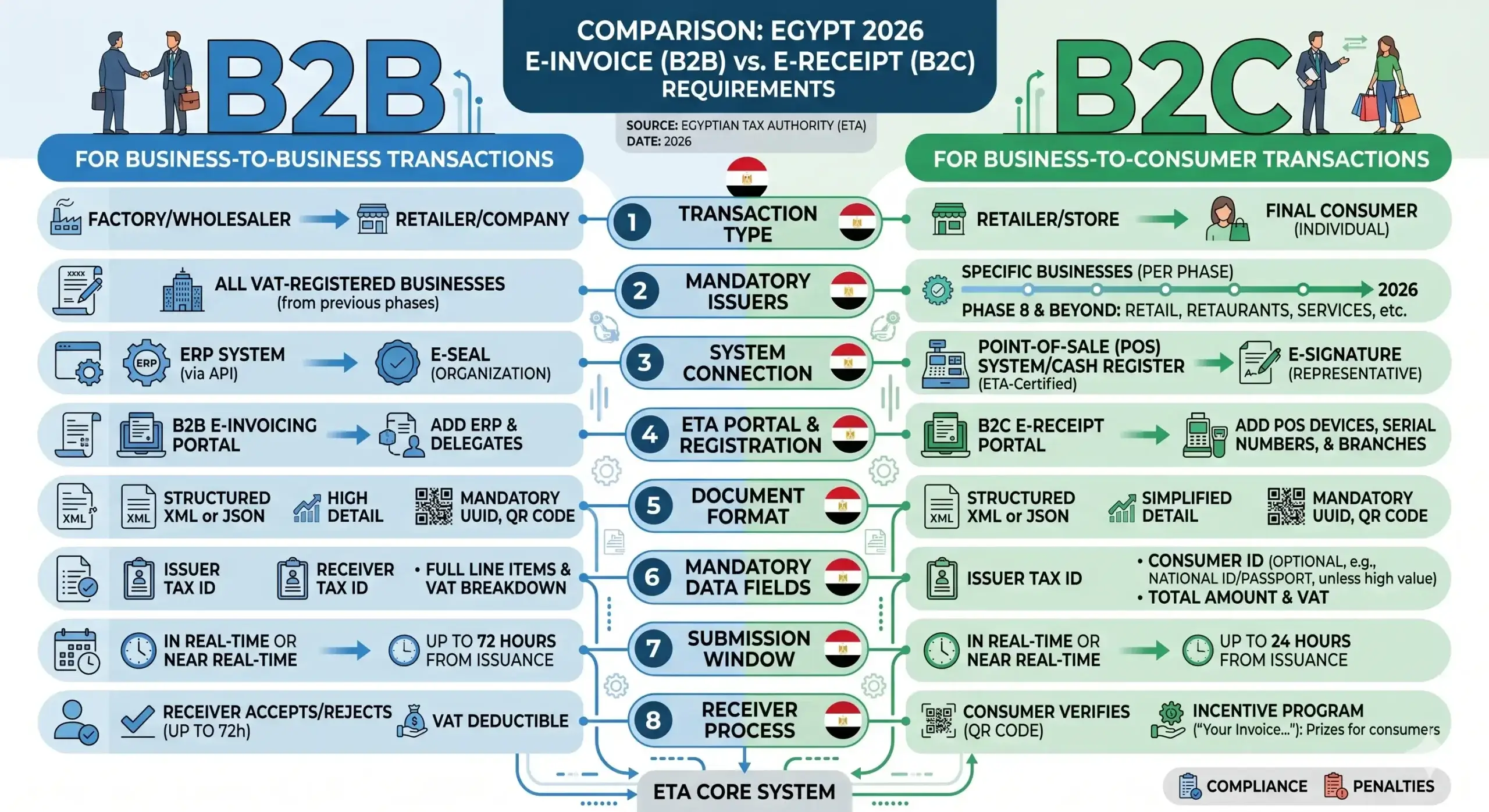

E-Invoice vs. E-Receipt: What’s the Difference?

Confusing these two systems is the single most common mistake in ETA integration projects. They are two separate platforms with different rules — and most businesses need both simultaneously.

| Attribute | E-Invoice | E-Receipt |

| Transaction Type | B2B / B2G (business-to-business) | B2C (business-to-consumer) |

| Submission Channel | ERP → ETA API directly | POS → ETA API at point of sale |

| Submission Timing | Real-time (same day) | Within 72 hours maximum |

| Format | XML or JSON | JSON via POS API |

| Digital Signature | Mandatory (HSM or USB Token) | Certified POS signature |

| UUID | Required per invoice | Required per receipt |

| QR Code | Available | Mandatory on print (2026) |

| Buyer Data | TIN + full address | Simplified (name only) |

| Retention Period | Minimum 5 years | Minimum 5 years |

When Do You Need Both Systems?

Most real-world businesses operate in both B2B and B2C channels simultaneously:

- Retail chains issue e-receipts to walk-in customers and e-invoices to corporate accounts and suppliers.

- Hospitals and clinics issue e-receipts to patients (B2C) and e-invoices to insurance companies (B2B).

- Manufacturers issue e-invoices to wholesale buyers and e-receipts at factory showrooms.

- E-commerce platforms issue e-receipts for consumer orders and e-invoices for business accounts.

Configuring only one system while your operation spans both creates immediate exposure — the transactions you miss accumulate as unreported revenue in ETA’s database.

Is Your Business Required to Register? The New EGP 250,000 Rule

The Core Rule

If your gross annual revenue exceeded EGP 250,000 in 2025, you are legally required to register with ETA before March 31, 2026.

Gross revenue means before expenses are deducted. For example: if you invoiced EGP 260,000 but your operating costs were EGP 240,000 (leaving a net profit of just EGP 20,000), you are still in scope. The threshold is triggered by revenue, not profit — and ETA cross-references your VAT filings against exemption claims automatically.

Newly In-Scope Categories in 2026

- Sole proprietorships and freelancers with revenue between EGP 250,000 and EGP 500,000.

- Service providers — consultants, independent software developers, small engineering and advisory firms.

- Multi-location retailers where the combined revenue of all branches exceeds the threshold.

- E-commerce merchants operating on Shopify, WooCommerce, or similar platforms.

- Government contractors (already covered separately under B2G rules, but now subject to the unified penalty system).

Limited Exceptions

- Small-scale farmers and fishermen may have temporary relief per ETA Circular No. 53/2023.

- Foreign companies without a permanent establishment or Egyptian VAT registration are not directly obligated — the burden shifts to the Egyptian customer via the Reverse Charge mechanism.

- Businesses with annual revenue below EGP 250,000 remain outside the mandate (but can voluntarily register).

⚠️ Critical Warning: ETA matches your declared revenue against your VAT filings automatically. Any inconsistency between what you report and what you claim as exempt triggers an automated tax audit within 30 days.

Critical Deadlines in 2026

| Date | Event | Who’s Affected |

| January 1, 2026 | Resolution 281/2025 and three-tier penalty regime take effect | All registered taxpayers |

| March 31, 2026 | Final registration deadline for businesses above EGP 250,000 | Newly in-scope SMEs |

| June 30, 2026 | End of grace period for corrections without penalties (in certain cases) | Late registrants |

| Ongoing | B2B invoices must be submitted in real-time | All B2B transactions |

| Ongoing | B2C receipts must be submitted within 72 hours | All B2C transactions |

Penalties for Non-Compliance

1. Non-Registration Penalties

- Immediate fine: EGP 20,000 upon crossing March 31, 2026, without registration.

- Daily compounding penalty: EGP 1,000 per day of delay until registration is completed.

2. Three-Tier Late Submission Regime

| Tier | Offense Count (Rolling 12 Months) | Penalty |

|---|---|---|

| Tier 1 | First offense | Warning flag on taxpayer profile (90 days) — no financial penalty |

| Tier 2 | Second offense | EGP 5,000 per late invoice (capped at EGP 50,000/month) + “High Risk” classification + quarterly audits instead of annual reviews |

| Tier 3 | Three or more offenses | EGP 10,000 per invoice (no cap) + potential suspension of invoicing capability entirely |

💡 The Hidden Trap: ETA counts each invoice as a separate offense. If you submit 200 late invoices in a single batch, that’s 200 separate violations — potentially EGP 2 million in penalties from one operational mistake under Tier 3.

3. Additional Consequences

- Loss of Input VAT deduction rights for any paper invoice issued after 2022.

- Exclusion from government contracts and public tenders.

- Import/export restrictions — non-compliant businesses cannot clear customs through the NAFEZA single-window platform.

- Criminal penalties of 3 to 5 years imprisonment in documented tax evasion cases.

Registration & Technical Integration: The Complete Path

This section is directed at IT managers and developers responsible for implementing the integration. If you’re a business owner, skim this section and share it with your tech team.

Step 1: Obtain Your Tax Registration Number (TRN)

If you’re not yet registered with ETA, visit the local tax office responsible for your business district with:

- A valid commercial registration certificate

- National ID cards for company owners

- Proof of business address (rental contract or ownership deed)

The TRN is typically issued within 3-5 business days. You cannot proceed to e-invoicing registration without it.

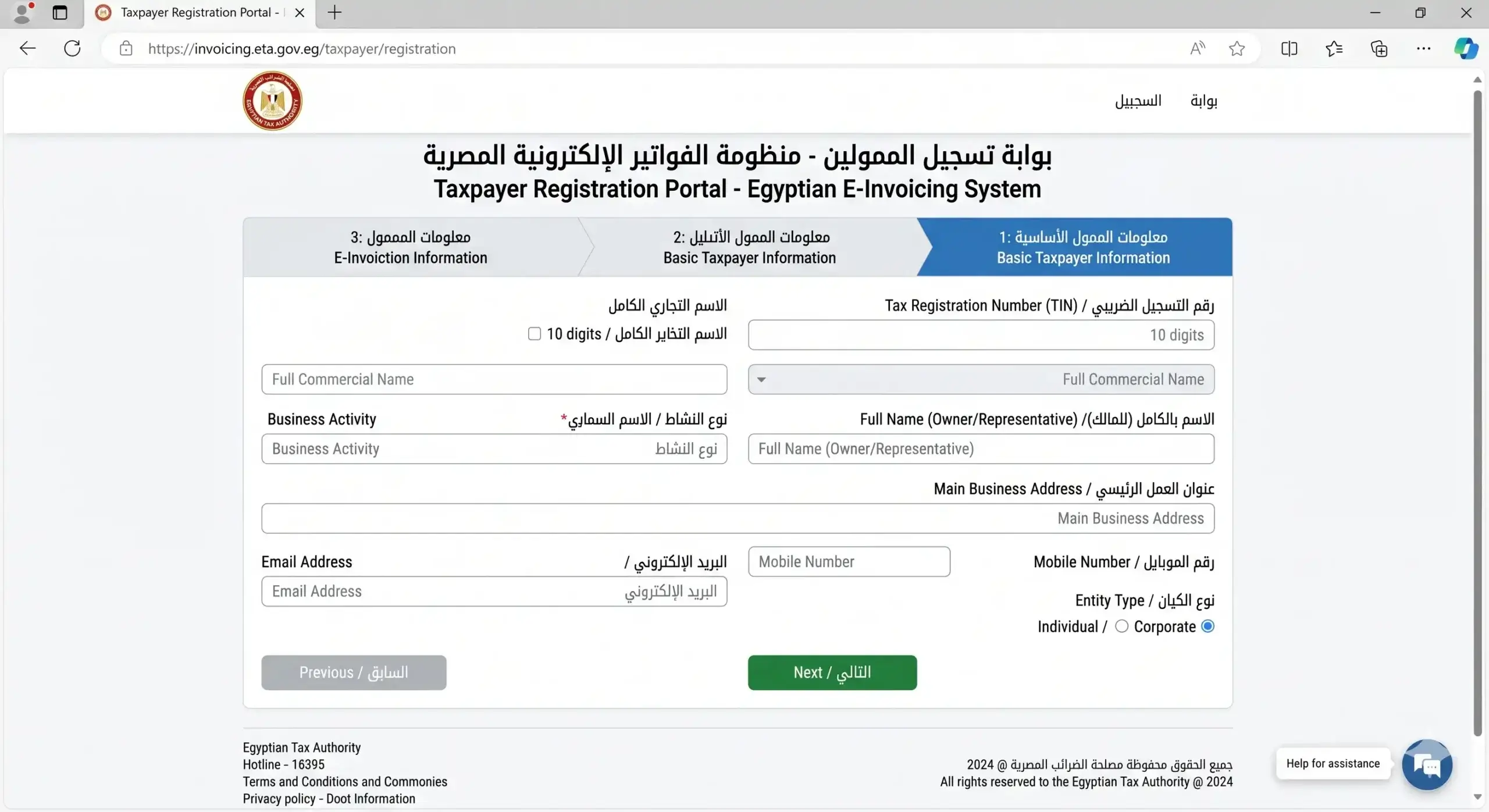

Step 2: Register on the ETA Portal

Go to invoicing.eta.gov.eg and create a Taxpayer Admin account. You’ll need:

- Your TRN

- Legal business name (must match the commercial registration exactly)

- Official contact email

ETA sends a temporary password to your email — change it immediately upon first login.

Step 3: Choose Your Digital Signature Method

You have three options, scaled to your invoice volume:

| Option | Cost (EGP) | Best For |

|---|---|---|

| USB Token | 2,000 – 3,500 | Under 500 invoices per month |

| HSM (Hardware Security Module) | 8,000 – 12,000 | Over 500 invoices/month, automated ERP issuance |

| Cloud Signing Service (e.g., OrchidaTax) | Monthly subscription | Businesses wanting SaaS with no hardware management |

Step 4: Product & Service Coding (GS1 / EGS)

Every product and service you sell must have a GPC (Global Product Classification) code aligned with GS1 international standards, or the local EGS code that maps your internal SKUs to the global taxonomy. This step is frequently overlooked and becomes the single biggest blocker during go-live. Budget at least 2-4 weeks for catalog classification.

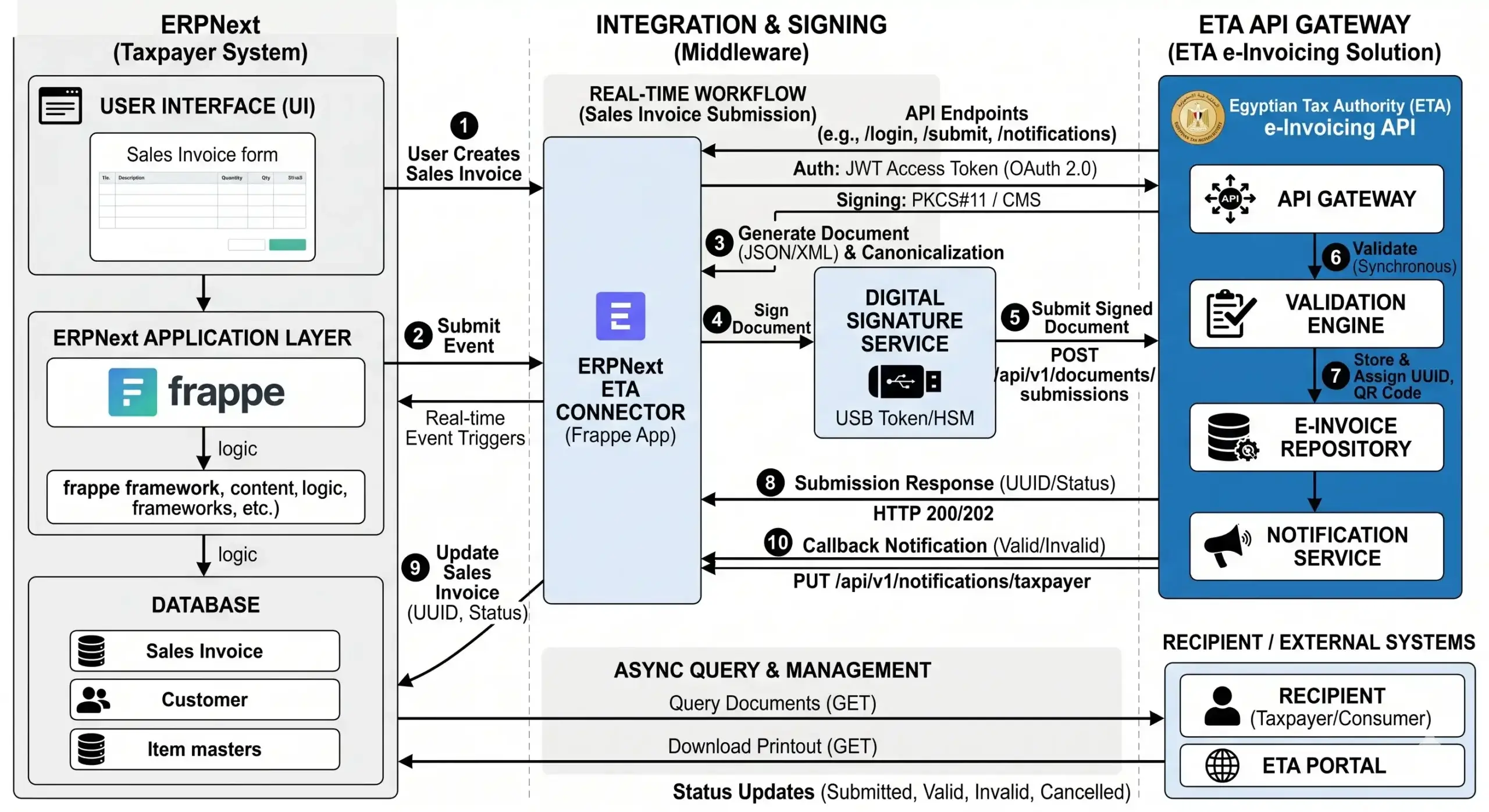

Step 5: Technical Integration with ETA API

Integration happens via a REST API, with invoices transmitted as XML or JSON payloads. The complete invoice lifecycle:

1. Invoice created in ERP and validated against ETA Schema

2. Digital signature applied via HSM or USB Token

3. Signed payload transmitted to ETA API endpoint

4. ETA returns a unique UUID upon successful validation

5. UUID linked to the invoice record in the ERP

6. Invoice made available to buyer (72 hours to accept or reject)

A few technical details that matter:

- Authentication uses OAuth 2.0 with client credentials flow.

- Rate limits apply on the ETA API — batch processing requires careful throttling.

- Schema versioning changes periodically; your integration must handle forward compatibility gracefully.

- Error responses are not always descriptive — log every request/response pair for debugging.

Step 6: Testing and Phased Rollout

Run the integration on the Preprod environment for a minimum of two weeks before production. Test every edge case: multi-currency invoices, credit notes, debit notes, rejected invoices, and partial submissions. Rushing this stage is the single most common cause of multi-million EGP penalty exposure in the first operational month.

How ERPNext Simplifies ETA Compliance

Businesses managing invoicing manually — whether on Excel, legacy accounting software, or paper-based systems — face three recurring problems with ETA: late submissions, schema validation errors, and difficulty reconciling sales with VAT filings.

ERPNext addresses these through three built-in mechanisms:

1. Direct Real-Time Integration with ETA API

When a sales invoice is submitted in ERPNext, it’s automatically transmitted to ETA at the same moment. The UUID returned by ETA is stored against the invoice record, with no manual copying or separate portal workflow. Your accounting team never touches the ETA portal for routine transactions.

2. Automated Digital Signing

Integration with cloud HSM services means every invoice is signed without human intervention. For businesses issuing dozens or hundreds of invoices daily, this eliminates the operational bottleneck of manual USB Token signing — a workflow that simply doesn’t scale past small retail volumes.

3. Automatic Reconciliation and Compliance Reporting

ERPNext provides monthly ETA reconciliation reports, alerts for rejected invoices, and flags for any invoice that didn’t receive a UUID. This prevents any submission from ever reaching Tier 2 of the penalty regime — because exceptions are caught within hours, not weeks.

🔗 Related Reading: ERPNext vs Odoo vs NetSuite: Which ERP Is Right for You?

Cross-Industry Experience

At Data Value Solutions, we’ve implemented ETA integration across multiple verticals, including trading, manufacturing, healthcare, and real estate. Each industry has unique schema challenges — a medical clinic requires different mandatory fields than a trading company, and multi-branch retail adds complexity around outlet-level reporting that generic integrations miss.

Quick Compliance Checklist: Before March 31, 2026

- Did your 2025 revenue exceed EGP 250,000?

- Do you have a valid Tax Registration Number (TRN)?

- Have you created a Taxpayer Admin account on the ETA portal?

- Have you acquired a USB Token or HSM for digital signing?

- Are all products and services coded with GS1/EGS classifications?

- Is your sales system (ERP or POS) integrated with the ETA API?

- Have you tested the full invoice lifecycle on the Preprod environment?

- Do you have electronic archival for invoices covering at least 5 years?

- Is your accounting team trained to interpret ETA rejection messages?

- Do you run a monthly reconciliation report between sales and ETA submissions?

If you answered “no” to any item, start immediately — your margin for testing is gone.

Frequently Asked Questions

Do I need to register for both the e-invoice and e-receipt systems?

Yes, if you sell to both businesses and consumers. The e-invoice system handles B2B transactions, while the e-receipt system handles B2C transactions. A retail business, for example, typically needs both.

What’s the difference between a USB Token and HSM?

A USB Token is a portable device requiring manual interaction for each signature — suitable for low volumes (under 500 invoices per month). An HSM is a server-side device that signs automatically without human intervention, essential for automated ERP-driven invoicing at higher volumes.

Are paper invoices still valid?

No. Since 2022, paper invoices have been legally invalid for Input VAT deduction or any tax purpose. ETA only recognizes properly signed electronic invoices.

How long must I archive electronic invoices?

At least 5 years per VAT Law No. 67 of 2016. Some tax advisors recommend 7 years as a safety buffer for late audits or disputes.

Can I issue invoices in foreign currencies?

Yes, but the VAT amount must be calculated and displayed in Egyptian Pounds (EGP) using the Central Bank’s official exchange rate on the issuance date.

What happens if ETA rejects my invoice?

You must correct the error and resubmit within the grace window. Rejected invoices are not counted in your VAT return and cannot be claimed as business expenses until successfully resubmitted.

Is my foreign company (without a permanent establishment in Egypt) required to comply?

Not directly. The obligation shifts to the Egyptian customer via the Reverse Charge mechanism. However, if you provide remote digital services to Egyptian consumers, you may be required to register under Ministerial Decree No. 160/2023.

What’s the approximate cost for a small business to get compliant?

For small operations:

- USB Token: EGP 2,000 – 3,500 (one-time)

- Accounting system modifications: varies by system

- If you use ERPNext with a pre-built ETA integration, costs are significantly lower than building the integration from scratch

Can I submit invoices manually through the ETA portal without integrating a system?

Yes, for small retailers issuing under 50 receipts per month. However, once you exceed 100 receipts monthly, manual entry becomes impractical and exposes you to 72-hour submission deadlines and Tier 2/Tier 3 penalties.

What’s the difference between ETA and ZATCA?

ETA is the Egyptian Tax Authority, while ZATCA is Saudi Arabia’s Zakat, Tax, and Customs Authority. Both enforce electronic invoicing mandates, but with different technical requirements (XML formats, certificates, APIs, QR structures). Companies operating in both markets need a system supporting both ZATCA and ETA requirements simultaneously.

Ready to Comply Before March 31, 2026?

Don’t wait until the final week. Registration alone takes several business days, and the technical integration requires weeks of testing before production deployment.

Book a free consultation with a Data Value ETA specialist — we’ll assess your current compliance gap, map out a registration roadmap, and show you exactly how ERPNext integrates with Egypt’s e-invoice and e-receipt systems to eliminate penalty exposure.

References & Official Sources

- Resolution No. 281 of 2025 — Egyptian Tax Authority

- Law No. 6 of 2025 — Simplified Tax Regime

- Unified Tax Procedures Law No. 206 of 2020

- VAT Law No. 67 of 2016

- Official ETA E-Invoicing Portal